How Cash Flow Waterfall Works in Project Finance

In project finance, control over cash flows determines who gets paid, when, and how much. This disciplined approach to cash management is one of the defining features of project finance. It directly influences sponsor returns, lender risk exposure, and overall investment outcomes.

This article explains how cash flow waterfall works, their typical structure, why they matter to lenders and investors, and the common mistakes that can undermine them.

What is a Cashflow Waterfall

A cash flow waterfall is a structured mechanism that determines how project revenues are distributed across different obligations. The concept is straightforward as cash flows through a defined order of priority, with each level fully paid before any funds move to the next. If cash is insufficient, lower-priority stakeholders simply do not get paid. While waterfalls vary by project type and lender requirements, most follow a common template with six to eight priority tiers. Understanding each component’s purpose and typical sizing provides the foundation for structuring and modelling effective waterfalls.

Priority 1: Operating Expenses and Taxes

Operating expenses receive absolute priority because projects cannot generate revenue without continuing operations. This tier includes routine operating costs (labour, utilities, materials, insurance), scheduled maintenance, and tax obligations. Lenders accept operating expense priority because failed operations destroy asset value and eliminate revenue entirely.

Priority 2: Senior Debt Service

After ensuring operational continuity, debt service claims priority both interest and scheduled principal payments. Most structures pay interest before principal, though some treat them equally. Debt service amounts are predetermined by amortization schedules, creating clarity around requirements. However, variable rate debt creates fluctuating interest costs, and sculpted amortization produces varying principal payments designed to match anticipated cash flow profiles.

Priority 3: Reserve Account Funding

Reserve accounts provide cushions against future uncertainties. The waterfall allocates cash to fill reserves to required levels before allowing junior payments. Common reserves include:

- Debt Service Reserve Account (DSRA): Typically, six months of projected debt service, providing a buffer if revenues temporarily decline.

- Major Maintenance Reserve: Funds periodic major overhauls based on engineering studies projecting equipment replacement schedules and costs.

- Working Capital Reserve: Covers timing mismatches between revenue receipts and operating expense payments.

Reserve levels create tension between lenders wanting extensive cushions and sponsors viewing reserves as unproductive cash.

Priority 4: Cash Sweep/Mandatory Prepayment

Many waterfalls include mandatory debt prepayment provisions that accelerate deleveraging when cash flows exceed scheduled debt service and reserve requirements. This tier captures excess cash, applying it to debt principal reduction. Cash sweep provisions often include conditional logic they may activate only when debt service coverage ratios fall below thresholds (commonly 1.20x-1.30x), providing lenders with accelerated deleveraging during stress periods.

Priority 5: Subordinated Debt Service (if applicable)

When capital structures include mezzanine or subordinated financing, these obligations receive priority over equity but rank below senior debt and reserves. Subordinated debt service follows senior debt service in the waterfall, creating intermediate claim rights that provide subordinated lenders protection superior to equity while accepting substantial subordination to senior lenders.

Priority 6: Equity Distributions

Finally, remaining cash distributes to sponsors as equity returns—the residual cash flow available after satisfying all senior obligations. Distributions are not guaranteed; they occur only when sufficient cash cascades through all senior tiers.

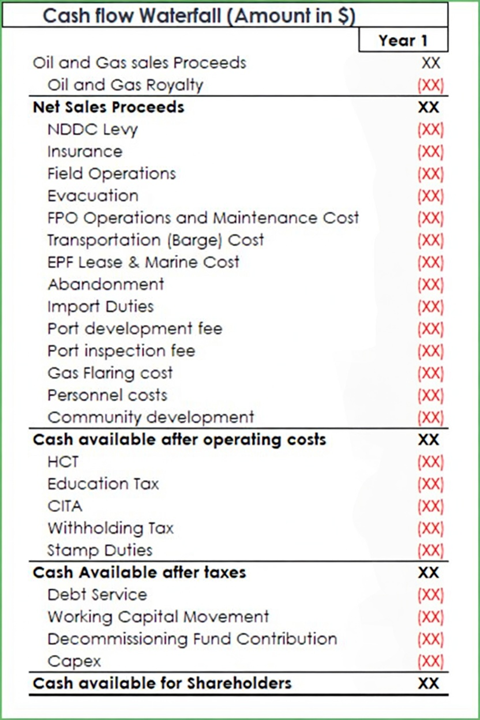

Figure 1: Illustrative Cashflow Waterfall

Why Waterfalls Matter to Lenders and Investors

From a lender’s perspective, the cash flow waterfall is a core risk control mechanism. It enforces strict payment priority, ensuring that debt service is met before any value flows to equity. By requiring reserve funding ahead of distributions, it builds buffers that protect against temporary revenue shortfalls. It also allows lenders to trap cash during periods of underperformance, accelerating deleveraging when coverage weakens. Just as importantly, it introduces transparency through defined calculations and monitoring rights, reducing the risk of cash leakage.

This level of control is one of the key reasons lenders are comfortable with limited recourse structures in project finance. Unlike corporate finance where management retains discretion over cash usage the waterfall removes that flexibility, replacing it with a disciplined, contract-driven system that prioritizes repayment.

For sponsors and investors, however, the implications are hugely different. The waterfall makes equity returns inherently uncertain. Distributions only occur after all senior obligations are met, creating a highly variable outcome. In impressive performance scenarios, excess cash can translate into significant returns. In more moderate cases, mandatory sweeps or reserve requirements may absorb most of the available cash. In weaker scenarios, distributions may stop entirely.

Common Issues and Structuring Mistakes

One common issue that can occurred when modelling a cashflow waterfall is overly complex structures. Some deals include too many tiers, sub-falls, and conditional rules, making them difficult to model, administer, and interpret. This often leads to errors and disputes. In practice, simpler structures with clearly defined tiers tend to work better. Another frequent problem is poorly calibrated reserve levels. Insufficient reserves leave projects exposed to short-term shocks, while excessive reserves trap cash unnecessarily and reduce efficiency. The right approach is to size reserves based on actual risk not arbitrary benchmarks.

Similarly, overly restrictive distribution conditions can prevent equity from being paid even when the project is performing well. If thresholds are set too high or conditions too rigid, the structure effectively delays or eliminates investor returns. Well-designed conditions should protect lenders without undermining the investment case.

Conclusion

Cash flow waterfalls are the practical backbone of project finance, translating risk allocation into clear payment priorities. They determine how cash is distributed, when stakeholders are paid, and how the project performs under stress. For sponsors, investors, lenders, and modelers, a well-designed waterfall directly shapes returns, risk exposure, and operational flexibility.

Strong waterfalls are simple, disciplined, and purpose driven. They prioritize essential obligations, use appropriately sized reserves, and apply conditional controls such as sweeps and distribution restrictions based on real performance indicators, not arbitrary rules. At the same time, they must strike a balance between protecting lenders during downside scenarios and allowing sponsors to benefit when the project performs well.